There are a number of differences in the content of financial statements for companies: terminology used, tax, dividends and the content of the financial statements. I will briefly mention the differences here and then we will look at some of them in more depth in later posts.

Terminology

As we move from considering unincorporated entities (sole traders and partnerships) to companies, the accounting terminology differs to bring company accounts in line with accounting standards.

Tax in company accounts

So far, tax has not played a part in any of the accounting statements that we considered for sole traders and partnerships. This is because partnerships and businesses run by sole traders do not have separate legal personality, and therefore do not pay tax. The partners or the sole trader pay tax by reference to their own personal tax computations.

Companies however do have a separate legal personality, and as such, they must pay tax on their own account. In practice, therefore, the Profit and Loss Account of a company includes a statement of the tax the company should pay on its profits. This is corporation tax and will ultimately affect the profitability of the company.

Dividends

The owners of companies are shareholders and the shareholders’ return on their investment is the dividend that they may receive.

Like drawings that a sole trader takes from his business, a dividend is an appropriation of profits (after tax). It is not an expense of the business. In practice, dividends will usually appear in a financial statement called the ‘statement of equity’ (or ‘statement of changes in equity’) because they are transactions between the company and its shareholders. Dividends are also sometimes included in an addition to the Balance Sheet called the Statement of Changes in Equity (SoCiE). This shows profits brought forward and added to current year profits subject to any deductions for dividends. The resulting ‘Retained Earnings’ will appear on the bottom half of the Balance Sheet, showing the total profits carried forward to the next accounting period.

Capital accounts: the bottom half of the balance sheet

Company accounts follow a format which differs from those of sole traders and partnerships. The main difference relates to the bottom half of the Balance Sheet and this is due to the fact that the capital of a company consists of share capital, reserves and retained earnings.

My previous posts on business accounts have discussed the format of the Profit and Loss Account and Balance Sheet for sole traders and partnerships, together with the necessity of making year-end adjustments such as accruals, prepayments, depreciation and bad and doubtful debts to the trial balance before producing the financial statements. These same principles also apply to companies, however there are some differences to the Profit and Loss Account and Balance Sheet of a company, which I will cover over the next few posts.

Regulation of company accounts

There are three main sources of regulation of UK company accounts:

The Companies Acts 1985, 1989 and 2006 (‘CA’);

Accounting standards; and

The FCA Listing Rules, Prospectus Rules and Disclosure and Transparency Rules (for companies whose securities are offered to the public in the UK or admitted to trading by the London Stock Exchange).

Companies prepare accounts because they are obliged to do so by statute. The accounts also have to take on a particular appearance and format and must also present a true and fair view of the profits, assets and liabilities of the company (s.396(2) CA 2006). This is because the accounts need to provide the reader, whether they are a shareholder, potential investor or an individual investigating an allegation of fraud, with certain key information. Unless that information is presented in a particular way, and consistently each year, then the story that the accounts actually tell may not be true or fair.

A company is free to choose its own accounting reference period, subject to provisions of the Companies Act 2006. Under s.391(4) CA 2006, a company’s accounting reference date (ARD) (the date on which the accounts are ‘ruled off’) is the last day of the month in which the anniversary of its incorporation falls. A company is, however, able to change its ARD to a date of its choice provided the provisions of s.392 CA 2006 are complied with. Under s.442(2)(a) CA 2006, a private company must file its accounts at Companies House within nine months after the end of the relevant accounting reference period and under s.442(2)(b) CA 2006, a public company must file its accounts at Companies House within six months after the end of the same period.

The main accounting requirements of the Companies Act 2006 are contained in Part XV and deal with matters such as:

the duty to keep accounting records (s.386 CA 2006);

accounting reference periods and accounting reference date (s.391-392 CA 2006);

the duty to prepare annual company accounts (s.396 CA 2006);

for parent companies, the duty to prepare group accounts (ss.399, 403 and 404 CA 2006). In principle, every subsidiary in a group remains subject to the duty to prepare its own individual accounts – but in practice many subsidiaries will qualify for an exemption from this;

the duty to prepare a directors’ report (ss.415- 419A CA 2006);

the duty to prepare an auditors’ report (ss.475, 495- 497A CA 2006);

the duty to provide every member with a copy of the accounts (s.423 CA 2006);

the duty for public companies to lay the accounts before a general meeting (ss.437-38 CA 2006); and

the duty to deliver copies of the accounts to the registrar (ss.441, 444- 447 CA 2006).

Accounting standards are issued as Financial Reporting Standards (‘FRSs’) by the Financial Reporting Council (www.frc.org.uk). They were formerly issued as Statements of Standard Accounting Practice (‘SSAPs’), some of which are still in force. Accounting standards apply to all companies.

As a consequence of the Companies Acts, FRSs and SSAPs, company accounts tend to conform to a given format, with a large number of supplementary notes (i.e. footnotes giving extra detail).

Some of the legal and regulatory requirements are relaxed in relation to ‘small’ or ‘medium-sized’ companies, as defined by statute (ss.382, 465 CA 2006). In addition, ‘micro-entities’ (very small companies) are exempt from certain financial reporting requirements, including in relation to s.396(2A) CA 2006.

In my previous articles on the subject of business accounts, I have focused on the accounts of sole traders. However, as you will be aware, these are not the only type of business entity that you may come into contact with in your role as a solicitor. I will now briefly move on to looking at the accounts of partnerships before we conclude with the accounts of companies.

Generally, the accounts of a partnership are very similar to those of a sole trader, having the same year-end adjustments. The main differences between the two is seen in the bottom half of the Balance Sheet (which you will recall denotes the capital held in the business). The reason for this is that in a partnership, the business will be owned by at least two different people. Therefore, to correctly show the capital of a partnership on the Balance Sheet, it is necessary to make an intermediate step in the preparation of the accounts. This is the preparation of a profit appropriation statement.

In short, the profit appropriation statement records the division of the profits of the business for the relevant accounting period between the partners.

Separate accounts for each partner

Within a partnership, each partner will have his or her own accounts, and commonly there are two accounts for each partner:

a Capital account, which represents the partner’s original investment in the partnership, together with any subsequent investments. This is long-term capital which cannot be withdrawn in normal circumstances.

a Current account, representing the capital that can be withdrawn at the partner’s discretion. This account records the partner’s share of the ongoing business profits. It will also show any drawings that the partner has taken out over the year.

Drawings are withdrawals of profits by the partners during the year, to pay themselves, in much the same way as sole traders pay themselves. The drawings are usually based on an estimate of the partner’s share of expected profits for the year. If a partner draws too much then they could be liable to make a balancing payment back to the partnership depending on the terms of the partnership agreement.

Appropriation of profits

Once the Profit and Loss account has been drawn up and the profit for the business as a whole has been calculated, the profit which the partnership has made needs to be divided amongst the partners. This is done as follows: firstly, sums are allocated to individual partners corresponding to any ‘interest’ on their capital or ‘salaries’ due to them under the partnership agreement. Then the residual profit will be distributed to the partners according to an agreed profit share ratio.

Notional interest on capital

The notional interest is a a payment representing interest on the capital in the partner’s long-term capital account. This will be calculated using a rate of interest that is specified in the partnership agreement. It is important to note that although it is labelled ‘interest’, it should not be treated as an expense item in the Profit and Loss Account. It is notional interest, i.e. it is really an appropriation of profit to a particular director under a different name.

Notional salary

One or more of the partners might receive a notional salary, which again will be in the partnership agreement and is also really an appropriation of profits. Generally, for partners, any salary paid to them:

must be treated as an appropriation of profit, not an expense in the Profit and Loss Account (which is how the salaries of any employees the partnership has would be represented); and

will be treated as drawings.

Residual profits

The residual profits are the profits for the period remaining after each partner has appropriated any amount(s), to which they are entitled as notional interest and/or notional salary. The residual profits are divided amongst the partners according to an agreed ratio, which will again be specified in the partnership agreement.

Profit appropriation statement

A profit appropriation statement is a practical way to work out the distribution of the profits and must be completed before the Balance Sheet can be drawn up. To complete a profit appropriation statement it is necessary to:

give each partner his/her appropriation of profit for notional salary and notional interest.

calculate how much profit is left over (the residual profit).

share this residual profit between the partners according to the profit-sharing ratio.

Example profit appropriation statement

Brown Design is a partnership of architects. The trial balance of the firm at 31 December 2020 included the following items:

Debit £

Credit £

Brown Capital account Current account Drawings

22,000

75,000 25,000

Smith Capital account Current account Drawings

30,000

82,000 35,000

Jones Capital account Current account Drawings

35,000

50,000 40,000

For the year ended 31 December Year 2, the partnership made a profit of £135,000 and the profits are shared as follows:

Brown is given a notional salary of £21,000 and Smith is given a notional salary of £26,000.

Each partner is paid interest on (long-term) capital of 5% p.a.

The partners share the residual profits in the ratio 5:3:2 to Brown: Smith: Jones.

Once this information has been obtained, the Profit Appropriation Statement can be drawn up as follows:

Partner

Notional salary £

Notional interest £

Share of residual profit £

Total share of profit £

Brown

21,000

3,750

38,825

63,575

Smith

26,000

4,100

23,295

53,395

Jones

2,500

15,530

18,030

47,000

10,350

77,650

135,000

Calculations: Notional Interest = 5% of £75,000 for Brown, 5% of £82,000 for Smith and 5% of £50,000 for Jones. Residual profit = £110,000 minus notional salaries (£47,000) and notional interest (£10,350). Residual profit = £77,650, divided 5/10 to Brown, 3/10 to Smith and 3/10 to Jones.

Partnership Balance Sheet

The top half of a partnership Balance Sheet is similar to that of a sole trader, but the bottom half, which shows capital, follows a different format:

the Balance Sheet shows the capital position for each partner separately;

the Balance Sheet shows each partner’s capital account and current account; and

the balance of each partner’s current account is adjusted by adding that partner’s total share of profit (as calculated in the profit appropriation table) and subtracting that partner’s drawings.

The example below shows the bottom half of the balance sheet for Brown Design based on the information given previously.

£

£

£

Brown:

Capital account

75,000

Current account

At start of year

25,000

Share of profit

63,575

Drawings

(22,000)

At end of year

66,575

Brown: total capital

141,575

Smith:

Capital account

82,000

Current account

At start of year

35,000

Share of profit

53,395

Drawings

(30,000)

At end of year

58,395

Smith: total capital

140,395

Jones:

Capital account

50,000

Current account

At start of year

40,000

Share of profit

18,030

Drawings

(35,000)

At end of year

23,030

Jones: total capital

73,030

Total partnership capital:

355,000

The total partnership capital would equal the Net Assets from the top half of the Balance Sheet.

In my two previous posts, I discussed bad debts and doubtful debts as separate considerations for year-end adjustments. In practice though, when it comes to preparing financial statements for a company, both adjustments would be made in one combined calculation. When adjusting for ‘bad and doubtful debts’, it is important that the receivables figures are adjusted first, This means that you must deduct any bad debts written off at the year-end first. This is necessary because any general provision for doubtful debts is calculated by applying a percentage to the balance of the receivables asset account. You will only know the correct balance on this account after you have adjusted for any bad debts written off at the year-end.

Adjustment for bad debts

When you are given a preliminary trial balance:

the receivables asset account will show the balance on the account before taking into account the bad debt written off at the end of theyear.

there may be a bad debt expense account, if the business has already written off bad debts during the course of the year and the receivables asset account (as it appears in the trial balance) will already have been reduced to take account of them.

To make the year-end adjustment for bad debts, you have to:

Deduct the amount of the bad debt from the receivables asset balance in the trial balance. The remainder constitutes the up-to-date figure for receivables and will appear on the balance sheet.

EITHER (if the trial balance already has a bad debts expense account) add the bad debt to the balance of the expense account OR (if the trial balance does not have a bad debts account) create a new expense account and show the bad debt as its balance.

Adjustment for doubtful debts

When you are given a preliminary trial balance:

the ‘Provision for Doubtful Debts’ account in the trial balance will show the provision for doubtful debts at the end of last year/start of the current year, so the actual figure shown on the trial balance is out-of-date and should not appear at all in the current year’s financial statements.

there will be no ‘Bad and Doubtful Debts’ expense account for the year shown on the trial balance. There may however be a ‘Bad Debts’ expense account, depending on whether or not bad debts have already been written off during the year.

To make the year-end adjustment for doubtful debts, you should:

calculate the current year end’s provision for doubtful debts figure (the ‘new provision figure’) in accordance with the method decided by the business itself. Eventually this figure will be shown on the balance sheet.

EITHER (where the new Provision for Doubtful Debts is more than the provision shown in the trial balance) add the amount by which the provision has increased to the (new or renamed) bad and doubtful debts expense account for the year OR (where the new Provision is less than the provision shown in the trial balance) subtract the amount by which the provision has decreased from the (new or renamed) bad and doubtful debts expense account for the year. The new provision figure is then shown in the ‘provision for doubtful debts’ liability account.

A doubtful debt occurs when a business provides for the possibility that a debt or debts may not be paid. The major difference between a doubtful debt and a bad debt is that the business is not writing off the doubtful debt completely. It is just making sure that the accounts accurately reflect the fact that the business possibly will not receive all of the money owed to it.

There are two possible ways being doubtful about debts:

Specific doubtful debts: A business may be aware that a particular debtor is in financial trouble, or has a debtor who disputing its liability to pay the debt. The debtor may not have entered into an insolvency process or the dispute may be settled on favourable terms, therefore, the business has not totally given up hope of receiving payment, but the business wants to show that it may not receive the amount owed.

General doubtful debts: A business may not have information on specific debts being doubtful, but perhaps knows that the market generally is not doing well and wants to make a general provision for a certain percentage of its debtors not to pay, e.g. it is estimated that 10% of its receivables may not be paid.

A business could decide to make a specific provision or a general provision, or a combination of both, to quantify its doubts and express them as an actual figure. This doubtful debt figure will be shown as the balance on an account called ‘Provision for Doubtful Debts’. The amount allocated to the provision for doubtful debts account is re-calculated at each year-end based on the business’ knowledge of its debts at that time. It might increase, reduce or stay the same compared with the previous year’s provision.

A provision account provides some cushioning for the business. Such an account can be viewed as a mechanism by which the business can ring-fence a certain amount of its net asset value, just in case it transpires that the doubtful debts need to be written off.

Showing Doubtful Debts as Expenses in the Profit and Loss Account

In future, a doubtful debt may be written off as a bad debt and become a real cost to the business. Because of this, doubtful debts are accounted for in the same expense account in the Profit and Loss Account as bad debts, a ‘Badand Doubtful Debts’ expense account.

As we saw previously, the ‘bad debts’ element of this account should be categorised as an expense because they represent a cost to the business. However, doubtful debts represent potential costs which the business may (or may not) incur. it would, therefore, be wrong to show the whole amount of a business’ provision for doubtful debts as an expense. Instead, only the increase (if any) in the provision for doubtful debts over the amount of the previous year’s provision is treated as an expense.

Provision for Doubtful Debts on the Balance Sheet

The Provision for Doubtful Debts is treated as a liability on the Balance Sheet. As a matter of presentation, it is shown in a different way from other liabilities and is ‘matched’ to the asset it most directly affects, the receivables asset account.

Example

Cocost Catering Wholesale (‘Cocost’) is a newly formed business, whose first accounting period ended on 31 December 2018.

Year end 2018 : At the end of 2018, Cocost’s receivables amount to £95,000. Cocost believes that one of its debtors, Burgerama Ltd (‘Burgerama’), is on the brink of insolvency and it is unlikely that they will pay their outstanding invoice of £750. Cocost makes a specific provision for doubtful debts for this £750.

In addition, Nightingales decides that it is likely that 2% of the remaining receivables may never be paid. Cocost therefore wishes to create a general provision of £1,885 for doubtful debts (£94,250,000 x 2% = £1,885).

So the total Provision for Doubtful Debts at the end of Year 2018 is £2,635.

As Cocost is a new business, the provision for doubtful debts at the start of Year 1 was £0. Therefore, at the end of Year 1 there has been an increase in the provision from £0 to £2,635. This means that the whole of this £2,635 increase is treated as an expense and must be included in the balance of the Bad and Doubtful Debts account in the Profit and Loss Account.

Year end 2019: When preparing the financial statements for 2019, Cocost decides that the total Provision for Doubtful Debts should be £3,250. This represents an increase of £615 from the previous year (£3,250 – £2,635= £615).

The increase of £500 is treated as an expense this year. By increasing its provision, in effect, Cocost is £615 ‘worse off’ than it was last year. Therefore, £615 is added to the Bad and Doubtful Debts Expense in the Profit and Loss Account.

Year end 2020: At the end of 2020, Cocost decides that trading conditions have improved and decides to reduce the total Provision for Doubtful Debts to £2,500.

A decrease in the Provision for Doubtful Debts reduces expenses. Therefore, when preparing the Profit and Loss Account for 2020, the Bad and Doubtful Debts expense is reduced by £750 (£3,250 – £2,500)

The accounts of sole traders show Debtors to the business, i.e. all of those who owe money to the business, each of which is a debtor to the business. In the accounts of partnerships and companies, the debtors are referred to as Receivables and again represents the money that the company is expecting to receive. Because this is money that the business is expecting to receive, the debtors/receivables is an asset account.

What are bad debts?

It is an unfortunate fact of business is that not all debts get paid and this has to be taken into account when preparing financial statements for a business.

A debt becomes a bad debt when the business knows with certainty that it is never going to receive payment of the amount owed. This could be, for example, because the debtor has gone into an insolvency/bankruptcy process. When this happens, the bad debt are written off. The owner of the business gives up any hope of collecting the debt and the debt is therefore removed from the Receivables/Debtors entry in the accounts.

Writing off bad debts

It may become apparent during the accounting year that a debt is never going to be paid and therefore, bad debts may be written off at any time during the accounting year. If they are written off during the accouting year then there will already be a bad debts expense account included in the trial balance. However, the business may also need to carry out a further year-end adjustment as other debts may be written off at the end of the accounting year when a review is performed of the debts that are owed to the business. If it is decided that a further debt needs writing off as a bad debt but the year-end adjustment is not performed, the accounts will not give a true reflection of the position of the business. Instead, it will seem that the business is expecting more money to be paid to it than is actually the case.

Dual effect of Bad debts

The effect of bad debts will be shown in an asset account and an expense account.

Asset: The receivables asset account will be reduced by the amount of the bad debt, resulting in the receivables account then show the correct balance. This is an adjustment to the balance sheet.

Expense: An expense account is used as the bad debt is a cost to the business. The business has supplied a product or service and will never be paid for it. This is an adjustment to the profit & loss account.

Example

At the end of its accounting period Jacksons Printers (‘Jacksons’) has a balance on its receivables account of £11,000. At year end it is discovered that one of its trade customers has been declared insolvent, owing Jacksons £550.

The trial balance will show that £11,000 is owing to Jacksons, but they know that £550 of that will never be paid.

The receivables asset account must therefore be reduced to £10,450 (i.e. £11,000 – £450).

The bad debt itself will be shown as part of a ‘bad and doubtful debts’ expense account.

A prepayment occurs when an expense is paid for in the current year but all or part of the cost should be charged as an expense next year. It therefore arises when a business has paid for something in advance during one accounting period but does not get the benefit of all or some of what it has paid for until the next. Therefore, it is in effect the ‘opposite’ of an accrual.

If an adjustment is not made for the prepayment then the accounts will not be giving a true reflection of the position of the business. If the business has paid for something but not yet received the benefit, then the profit of the business will be artificially low.

Dual effect of prepayments

Prepayments are recorded in an expense account and an asset account.

Expense: The relevant expense account is reduced so that it records the correct amount of ‘benefit’ used in the accounting period.

Asset: An asset account is created because the business has paid certain sums in advance and can look forward to receiving the benefit in the next accounting period.

Prepayment year-end adjustment

When you are given a preliminary trial balance:

the relevant expense account will show the balance on the account before taking into account the prepayment.

there will be no prepayment current asset account for the year in the list of account balances.

To make the year-end adjustment for prepayments, you should therefore:

deduct the amount of the prepayment from the relevant expense account in the trial balance. The reduced expense will be included in the profit & loss account; and

include the amount of the prepayment as a current asset in the balance sheet.

Example Blooms Florists (‘Blooms’) has paid £24,000 rent for its new shop. The rent was paid on 1 September when they moved in to the shop, for 12 months in advance. Blooms has an accounting year end of 31 December.

The trial balance will show that Blooms has paid £24,000 of rent in the accounting year. However, Blooms should only be paying rent in the present accounting period for the four months of September, October, November and December (i.e. £8,000, ((£24,000 ÷ 12 months) x 4 months)). The rest of the £24,000 (£16,000) should be accounted for in the next accounting period. The figure of £16,000 is the amount that Blooms has prepaid in respect of rent.

The correct figure of £8,000 must be shown in the Rent expense account on the Profit and Loss Account.

The £16,000 (i.e. the amount of the prepayment) will be shown in a Prepayment current asset account on the Balance Sheet since the business has yet to enjoy the benefit of the rent already paid.

An accrual occurs when an expense has been incurred and should be charged against profit in the current year but for some reason by the time the accounts are drawn up, that expense has not been included in the trial balance. This could be because the business has received the benefit of goods or services, but has not received an invoice for them.

Making an adjustment in this way complies with the accruals concept referred to above, because if an adjustment is not made for an accrual then the accounts will not be giving a true reflection of the position of the business for that year. The business will have had the benefit of something but not yet paid for it. Therefore, the profit of the business will be shown as artificially high unless the adjustment is made.

Dual effect of accruals

Accruals are recorded in an expense account and a liability account:

Expense: The relevant expense account is adjusted (in an upwards direction) so that it records the correct amount of goods, services (or other ‘benefit’) used in the accounting period.

Liability: A liability account is created, as the business has not yet paid the amount accrued and so we cannot reduce any asset directly. The liability account shows the business is liable to pay the amount of the accrual. All accruals are added together and shown in a single liability account (labelled ‘Accruals’).

Accruals year-end adjustment

When you are given a preliminary trial balance:

the relevant expense account will show the balance on the account before taking into account the accrual; and

there will be no accruals current liability account for the year in the list of account balances.

To make the year-end adjustment for accruals, you should therefore :

add the amount of the accrual/accrued expense to the expense account for that item in the trial balance. The increased expense figure will be included in the profit & loss account; and

include the amount of the accrual as a current liability in the balance sheet.

Example Town & County Auctioneers (‘TC’) recently moved to new premises and used the services of its solicitors, to act on its behalf for the purchase of the new property. The preliminary trial balance includes a balance of £6,500 in the Legal Fees account, which were fees that the company was billed for and has paid.

At the year end, TC has not yet received a bill of costs for some of the work done by the solicitors a month ago. The bill is expected to be for £500.

The trial balance shows that TC has used £6,500 of legal advice in the accounting year when really it has used £7,000 (i.e. £6,500 + £500) of legal advice.

The figure of £7,000 (including the £500 which TC has not yet paid for) must be included in the Legal Fees expense account and shown in the Profit and Loss Account.

The £500 which Panache owes must be included as an Accrual current liability account, and shown on the Balance Sheet.

A fixed asset (which max be referred to as a ‘non-current asset’ for a company) may have a useful life of several years, after which time it may be of little or no value. Depreciation is a mechanism used in the accounts to deal with this decline in value and to spread the cost of the asset over its useful life.

If depreciation were not used, the accounts would not give a true reflection of the position of the business. The assets would be stated at their cost value, which may, over time, be well above their actual value.

Depreciation has to be carried out in a systematic way, but the method used should mirror as closely as possible how the asset loses value in the course of the relevant accounting periods. The method that is ultimately chosen will depend not only on how the asset loses value but how it produces revenue for the business on an ongoing basis. As you will see below, an asset such as shelving will use the straight-line method because the asset is being used up consistently over its lifespan and is generating a consistent amount of income. But an asset such as a van, however, will produce much more revenue for the business in its earlier years of use and hence the reducing balance method will be more relevant. This amount is known as the ‘charge to depreciation’ or ‘depreciation charge’.

Depreciation methods

There are two common ways used to depreciate assets, the Straight-line method and the Reducing balance method.

Straight-line method

The straight-line method of depreciation spreads the depreciation charge evenly over the life of the asset and gives rise to the same charge for depreciation each year.

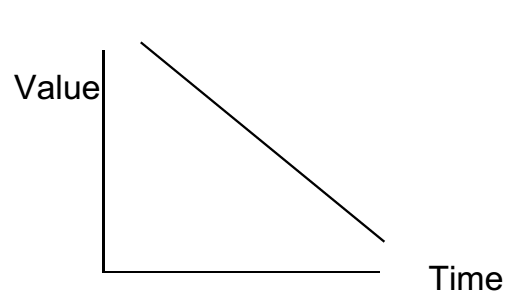

This is the most common and straightforward method of depreciation and is used where the service provided by the asset continues throughout its useful economic life on a consistent basis. If plotted on a graph, the depreciation of the asset would form a straight line.

Example Q&B DIY Store buys some shelving for its warehouse, costing £10,000. The shelving is expected to last for 5 years. The cost will be spread evenly over the five year period. A depreciation charge of £2,000 (i.e. £10,000 ÷ 5) will be made each year. This annual depreciation charge will ‘accumulate’ over the years. In year one, the accumulated charge will be £2,000, year two £4,000, year three £6,000 etc.

The charge each year (i.e. £1,200 in the example above) will be included in a depreciation account as the loss in value of the shelving constitutes a ‘cost’ to the business and will be shown on the Profit and Loss Account as an expense.

The accumulated depreciation will be included in an accumulateddepreciation account (liability account) thereby reducing the net book value of the asset and will be shown on the Balance Sheet. In the example given above, the accumulated depreciation after Year 3 will be £6,000.

Reducing balance method

The depreciation charge each year is expressed as a percentage (x %) of the reducing balance (i.e. the net book value of the asset at the start of the relevant accounting period). This means that more depreciation is charged in earlier years than in later years since the net book value of the asset reduces year on year.

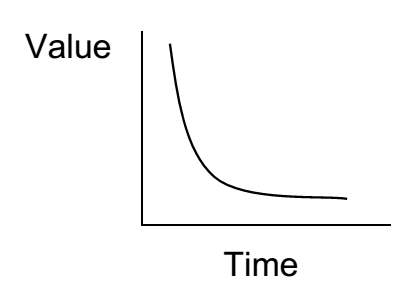

This method is less common and slightly more complicated than the straight-line method. The reducing balance method would be used where an asset is likely to lose a large part of its value in the first few years of ownership e.g. motor vehicles. If plotted on a graph the depreciation of the asset would form a curved line.

Example Sparks Electricians buys a van for £15,000 for use in the business. The van will be depreciated at a rate of 20% of the reducing balance each year.

At the end of Year 1, a depreciation charge of £3,000 (i.e. 20% of £15,000) will be made. This will be shown as an expense on the Profit and Loss Account for that year. It will also appear as a liability on the Balance Sheet, set off against the purchase (or cost) value of the van.

At the end of Year 2, the depreciation charge will be calculated as follows: the accumulated depreciation for the previous year (£3,000) is deducted from the cost of the asset in the trial balance. In this case the calculation will be £15,000 – £3,000 = £12,000. This figure of £12,000 is the reduced balance. The depreciation charge for Year 2 is calculated by applying the depreciation rate (20%) to the reduced balance (£12,000). This gives a depreciation charge for Year 2 of £2,400. This will be shown as an expense on the Profit and Loss Account for the second year. The accumulated charge at the end of Year 2 is £5,400 (£3,000 + £2,400) and this appears on the Balance Sheet as a liability.

At the end of Year 3, a depreciation charge of £1,920 (i.e. 20% of (£15,000 – £5,400) will be made. This will be shown as an expense on the Profit and Loss Account for Year 3. The Balance Sheet as at the end of Year 3 will show accumulated depreciation of £7,320.

Dual effect of depreciation

As we have seen above, depreciation is recorded in an expense account and a liability account.

Expense: An expense account is used because depreciation is an expense of the business each year, indicating that its assets are falling in value. The depreciation charge for each year will be shown in a depreciation account on the Profit and Loss Account.

Liability: The liability account accumulates all the annual expenses (as seen above). It has the effect of reducing the particular asset account. The accumulated depreciation will be shown in an accumulated depreciation account on the Balance Sheet.

Net Book Value

Fixed (or non-current) assets are recorded at the top of the Balance Sheet. The original cost of the asset is shown, as is the accumulated depreciation relating to that asset. A calculation is then performed to show the current value of the asset after taking into account its loss of value due to depreciation.

COST – ACCUMULATED DEPRECIATION = NET BOOK VALUE

The Net Book Value of an asset is an estimate of the current value of the asset to the business.

Depreciation year-end adjustment

When you are given a preliminary trial balance, there will be no depreciation charge for the current year in the trial balance; and the figure in the Provision for Depreciation account shown in the trial balance is the accumulated depreciation from previous years before charging depreciation for the current year.

To make the year-end adjustment for depreciation, you have to:

calculate the depreciation charge for the year and include it in the list of expenses; and

add the depreciation charge for the year to the accumulated provision for depreciation account.

Before the financial statements for an accounting period can be prepared, it is necessary to make some year-end adjustments to the trial balance. Year-end adjustments are transactions or modifications to the account entries on the trial balance. These are necessary to ensure that the accruals concept is applied to the preparation of the financial statements.

The accruals concept requires that:

all income and expenditure must be ‘matched’ to the relevant accounting period; and

all current obligations must be anticipated as liabilities and all asset values must be assessed to make sure they can be recovered through future profits in conditions of uncertainty.

For example, if a business’s accounting period matches the calendar year and it pays a year’s rent in advance on 1 September, only part of this payment will correspond to the current accounting period (1 Sept. – 31 Dec.). The remaining portion(1 Jan – 30 Aug.) will relate to the subsequent accounting period. According to the unadjusted trial balance, it will seem that the business has spent a lot more on rent for the current accounting period than it really has. The adjustments made effectively ‘correct’ this imbalance.

So if the rental payment made on 1 September was £12,000, only one-third of that figure (i.e. £4,000) will actually need to be shown in the financial statements for this year. The other £8,000 will be accounted for next year. This would be an example of a prepayment, as we will discuss later.

There are five year-end adjustments that you need to know, which you may need to carry out during the BLP exam: