The accounts of sole traders show Debtors to the business, i.e. all of those who owe money to the business, each of which is a debtor to the business. In the accounts of partnerships and companies, the debtors are referred to as Receivables and again represents the money that the company is expecting to receive. Because this is money that the business is expecting to receive, the debtors/receivables is an asset account.

What are bad debts?

It is an unfortunate fact of business is that not all debts get paid and this has to be taken into account when preparing financial statements for a business.

A debt becomes a bad debt when the business knows with certainty that it is never going to receive payment of the amount owed. This could be, for example, because the debtor has gone into an insolvency/bankruptcy process. When this happens, the bad debt are written off. The owner of the business gives up any hope of collecting the debt and the debt is therefore removed from the Receivables/Debtors entry in the accounts.

Writing off bad debts

It may become apparent during the accounting year that a debt is never going to be paid and therefore, bad debts may be written off at any time during the accounting year. If they are written off during the accouting year then there will already be a bad debts expense account included in the trial balance. However, the business may also need to carry out a further year-end adjustment as other debts may be written off at the end of the accounting year when a review is performed of the debts that are owed to the business. If it is decided that a further debt needs writing off as a bad debt but the year-end adjustment is not performed, the accounts will not give a true reflection of the position of the business. Instead, it will seem that the business is expecting more money to be paid to it than is actually the case.

Dual effect of Bad debts

The effect of bad debts will be shown in an asset account and an expense account.

Asset: The receivables asset account will be reduced by the amount of the bad debt, resulting in the receivables account then show the correct balance. This is an adjustment to the balance sheet.

Expense: An expense account is used as the bad debt is a cost to the business. The business has supplied a product or service and will never be paid for it. This is an adjustment to the profit & loss account.

Example

At the end of its accounting period Jacksons Printers (‘Jacksons’) has a balance on its receivables account of £11,000. At year end it is discovered that one of its trade customers has been declared insolvent, owing Jacksons £550.

The trial balance will show that £11,000 is owing to Jacksons, but they know that £550 of that will never be paid.

The receivables asset account must therefore be reduced to £10,450 (i.e. £11,000 – £450).

The bad debt itself will be shown as part of a ‘bad and doubtful debts’ expense account.

A prepayment occurs when an expense is paid for in the current year but all or part of the cost should be charged as an expense next year. It therefore arises when a business has paid for something in advance during one accounting period but does not get the benefit of all or some of what it has paid for until the next. Therefore, it is in effect the ‘opposite’ of an accrual.

If an adjustment is not made for the prepayment then the accounts will not be giving a true reflection of the position of the business. If the business has paid for something but not yet received the benefit, then the profit of the business will be artificially low.

Dual effect of prepayments

Prepayments are recorded in an expense account and an asset account.

Expense: The relevant expense account is reduced so that it records the correct amount of ‘benefit’ used in the accounting period.

Asset: An asset account is created because the business has paid certain sums in advance and can look forward to receiving the benefit in the next accounting period.

Prepayment year-end adjustment

When you are given a preliminary trial balance:

the relevant expense account will show the balance on the account before taking into account the prepayment.

there will be no prepayment current asset account for the year in the list of account balances.

To make the year-end adjustment for prepayments, you should therefore:

deduct the amount of the prepayment from the relevant expense account in the trial balance. The reduced expense will be included in the profit & loss account; and

include the amount of the prepayment as a current asset in the balance sheet.

Example Blooms Florists (‘Blooms’) has paid £24,000 rent for its new shop. The rent was paid on 1 September when they moved in to the shop, for 12 months in advance. Blooms has an accounting year end of 31 December.

The trial balance will show that Blooms has paid £24,000 of rent in the accounting year. However, Blooms should only be paying rent in the present accounting period for the four months of September, October, November and December (i.e. £8,000, ((£24,000 ÷ 12 months) x 4 months)). The rest of the £24,000 (£16,000) should be accounted for in the next accounting period. The figure of £16,000 is the amount that Blooms has prepaid in respect of rent.

The correct figure of £8,000 must be shown in the Rent expense account on the Profit and Loss Account.

The £16,000 (i.e. the amount of the prepayment) will be shown in a Prepayment current asset account on the Balance Sheet since the business has yet to enjoy the benefit of the rent already paid.

An accrual occurs when an expense has been incurred and should be charged against profit in the current year but for some reason by the time the accounts are drawn up, that expense has not been included in the trial balance. This could be because the business has received the benefit of goods or services, but has not received an invoice for them.

Making an adjustment in this way complies with the accruals concept referred to above, because if an adjustment is not made for an accrual then the accounts will not be giving a true reflection of the position of the business for that year. The business will have had the benefit of something but not yet paid for it. Therefore, the profit of the business will be shown as artificially high unless the adjustment is made.

Dual effect of accruals

Accruals are recorded in an expense account and a liability account:

Expense: The relevant expense account is adjusted (in an upwards direction) so that it records the correct amount of goods, services (or other ‘benefit’) used in the accounting period.

Liability: A liability account is created, as the business has not yet paid the amount accrued and so we cannot reduce any asset directly. The liability account shows the business is liable to pay the amount of the accrual. All accruals are added together and shown in a single liability account (labelled ‘Accruals’).

Accruals year-end adjustment

When you are given a preliminary trial balance:

the relevant expense account will show the balance on the account before taking into account the accrual; and

there will be no accruals current liability account for the year in the list of account balances.

To make the year-end adjustment for accruals, you should therefore :

add the amount of the accrual/accrued expense to the expense account for that item in the trial balance. The increased expense figure will be included in the profit & loss account; and

include the amount of the accrual as a current liability in the balance sheet.

Example Town & County Auctioneers (‘TC’) recently moved to new premises and used the services of its solicitors, to act on its behalf for the purchase of the new property. The preliminary trial balance includes a balance of £6,500 in the Legal Fees account, which were fees that the company was billed for and has paid.

At the year end, TC has not yet received a bill of costs for some of the work done by the solicitors a month ago. The bill is expected to be for £500.

The trial balance shows that TC has used £6,500 of legal advice in the accounting year when really it has used £7,000 (i.e. £6,500 + £500) of legal advice.

The figure of £7,000 (including the £500 which TC has not yet paid for) must be included in the Legal Fees expense account and shown in the Profit and Loss Account.

The £500 which Panache owes must be included as an Accrual current liability account, and shown on the Balance Sheet.

A fixed asset (which max be referred to as a ‘non-current asset’ for a company) may have a useful life of several years, after which time it may be of little or no value. Depreciation is a mechanism used in the accounts to deal with this decline in value and to spread the cost of the asset over its useful life.

If depreciation were not used, the accounts would not give a true reflection of the position of the business. The assets would be stated at their cost value, which may, over time, be well above their actual value.

Depreciation has to be carried out in a systematic way, but the method used should mirror as closely as possible how the asset loses value in the course of the relevant accounting periods. The method that is ultimately chosen will depend not only on how the asset loses value but how it produces revenue for the business on an ongoing basis. As you will see below, an asset such as shelving will use the straight-line method because the asset is being used up consistently over its lifespan and is generating a consistent amount of income. But an asset such as a van, however, will produce much more revenue for the business in its earlier years of use and hence the reducing balance method will be more relevant. This amount is known as the ‘charge to depreciation’ or ‘depreciation charge’.

Depreciation methods

There are two common ways used to depreciate assets, the Straight-line method and the Reducing balance method.

Straight-line method

The straight-line method of depreciation spreads the depreciation charge evenly over the life of the asset and gives rise to the same charge for depreciation each year.

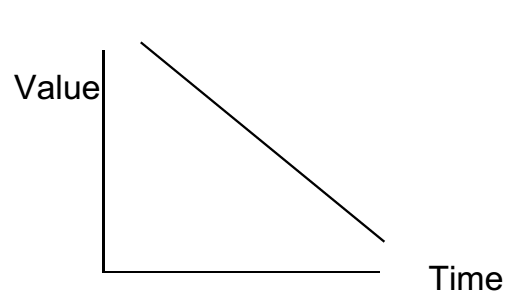

This is the most common and straightforward method of depreciation and is used where the service provided by the asset continues throughout its useful economic life on a consistent basis. If plotted on a graph, the depreciation of the asset would form a straight line.

Example Q&B DIY Store buys some shelving for its warehouse, costing £10,000. The shelving is expected to last for 5 years. The cost will be spread evenly over the five year period. A depreciation charge of £2,000 (i.e. £10,000 ÷ 5) will be made each year. This annual depreciation charge will ‘accumulate’ over the years. In year one, the accumulated charge will be £2,000, year two £4,000, year three £6,000 etc.

The charge each year (i.e. £1,200 in the example above) will be included in a depreciation account as the loss in value of the shelving constitutes a ‘cost’ to the business and will be shown on the Profit and Loss Account as an expense.

The accumulated depreciation will be included in an accumulateddepreciation account (liability account) thereby reducing the net book value of the asset and will be shown on the Balance Sheet. In the example given above, the accumulated depreciation after Year 3 will be £6,000.

Reducing balance method

The depreciation charge each year is expressed as a percentage (x %) of the reducing balance (i.e. the net book value of the asset at the start of the relevant accounting period). This means that more depreciation is charged in earlier years than in later years since the net book value of the asset reduces year on year.

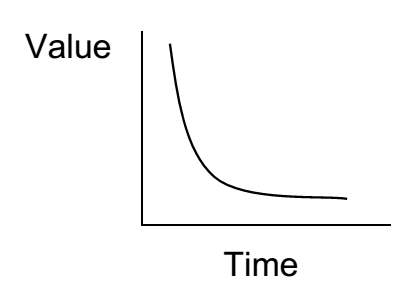

This method is less common and slightly more complicated than the straight-line method. The reducing balance method would be used where an asset is likely to lose a large part of its value in the first few years of ownership e.g. motor vehicles. If plotted on a graph the depreciation of the asset would form a curved line.

Example Sparks Electricians buys a van for £15,000 for use in the business. The van will be depreciated at a rate of 20% of the reducing balance each year.

At the end of Year 1, a depreciation charge of £3,000 (i.e. 20% of £15,000) will be made. This will be shown as an expense on the Profit and Loss Account for that year. It will also appear as a liability on the Balance Sheet, set off against the purchase (or cost) value of the van.

At the end of Year 2, the depreciation charge will be calculated as follows: the accumulated depreciation for the previous year (£3,000) is deducted from the cost of the asset in the trial balance. In this case the calculation will be £15,000 – £3,000 = £12,000. This figure of £12,000 is the reduced balance. The depreciation charge for Year 2 is calculated by applying the depreciation rate (20%) to the reduced balance (£12,000). This gives a depreciation charge for Year 2 of £2,400. This will be shown as an expense on the Profit and Loss Account for the second year. The accumulated charge at the end of Year 2 is £5,400 (£3,000 + £2,400) and this appears on the Balance Sheet as a liability.

At the end of Year 3, a depreciation charge of £1,920 (i.e. 20% of (£15,000 – £5,400) will be made. This will be shown as an expense on the Profit and Loss Account for Year 3. The Balance Sheet as at the end of Year 3 will show accumulated depreciation of £7,320.

Dual effect of depreciation

As we have seen above, depreciation is recorded in an expense account and a liability account.

Expense: An expense account is used because depreciation is an expense of the business each year, indicating that its assets are falling in value. The depreciation charge for each year will be shown in a depreciation account on the Profit and Loss Account.

Liability: The liability account accumulates all the annual expenses (as seen above). It has the effect of reducing the particular asset account. The accumulated depreciation will be shown in an accumulated depreciation account on the Balance Sheet.

Net Book Value

Fixed (or non-current) assets are recorded at the top of the Balance Sheet. The original cost of the asset is shown, as is the accumulated depreciation relating to that asset. A calculation is then performed to show the current value of the asset after taking into account its loss of value due to depreciation.

COST – ACCUMULATED DEPRECIATION = NET BOOK VALUE

The Net Book Value of an asset is an estimate of the current value of the asset to the business.

Depreciation year-end adjustment

When you are given a preliminary trial balance, there will be no depreciation charge for the current year in the trial balance; and the figure in the Provision for Depreciation account shown in the trial balance is the accumulated depreciation from previous years before charging depreciation for the current year.

To make the year-end adjustment for depreciation, you have to:

calculate the depreciation charge for the year and include it in the list of expenses; and

add the depreciation charge for the year to the accumulated provision for depreciation account.

Before the financial statements for an accounting period can be prepared, it is necessary to make some year-end adjustments to the trial balance. Year-end adjustments are transactions or modifications to the account entries on the trial balance. These are necessary to ensure that the accruals concept is applied to the preparation of the financial statements.

The accruals concept requires that:

all income and expenditure must be ‘matched’ to the relevant accounting period; and

all current obligations must be anticipated as liabilities and all asset values must be assessed to make sure they can be recovered through future profits in conditions of uncertainty.

For example, if a business’s accounting period matches the calendar year and it pays a year’s rent in advance on 1 September, only part of this payment will correspond to the current accounting period (1 Sept. – 31 Dec.). The remaining portion(1 Jan – 30 Aug.) will relate to the subsequent accounting period. According to the unadjusted trial balance, it will seem that the business has spent a lot more on rent for the current accounting period than it really has. The adjustments made effectively ‘correct’ this imbalance.

So if the rental payment made on 1 September was £12,000, only one-third of that figure (i.e. £4,000) will actually need to be shown in the financial statements for this year. The other £8,000 will be accounted for next year. This would be an example of a prepayment, as we will discuss later.

There are five year-end adjustments that you need to know, which you may need to carry out during the BLP exam:

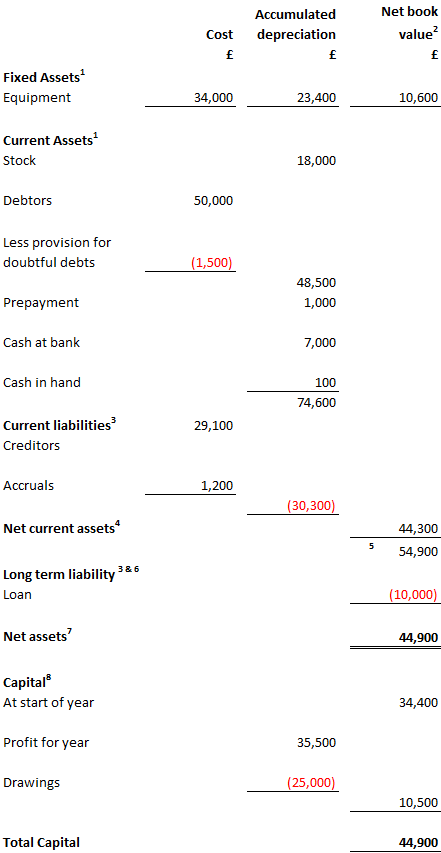

Below is an example of a balance sheet for the fictitious company ABC Trading, together with notes about it.

Notes for the Balance Sheet The Balance Sheet is in two parts. The top part shows all the liability accounts being deducted from all the asset accounts. The bottom part shows all the capital accounts of the business (i.e. money invested in the business) and importantly, includes the final profit figure from the Profit and Loss Account.

A distinction is made between ‘fixed’ assets and ‘current’ assets. ‘Fixed’ assets are held in the business long-term, such as land and buildings, machinery, etc. ‘Current’ assets come and go in the short term: a ‘current’ asset is one which is likely to be converted into cash within one year (e.g. when a debtor pays his bill).

The fixed assets of the business are set out at the top of the Balance Sheet. You will note that a horizontal format is used here, showing depreciation of these assets (the decline in their value since purchase). The Net Book Value figure (£10,600) in the right hand column represents the cost of acquiring the asset less depreciation. It is this figure that is used in calculating the Net Asset Value (‘NAV’) of the business.

Liabilities are categorised in a similar way to assets, as either ‘current’ or ‘long term’. ‘Current’ liabilities are due to be paid within one year, ‘long term’ liabilities after at least a year.

A sub-calculation is now performed to show the ‘Net Current Assets’ of the business. This figure is calculated by deducting all current liabilities from all current assets (i.e. ignoring fixed assets and long-term liabilities). The Net Current Asset figure (£44,300 in this example) is shown in the right hand column and is used in calculating the NAV. Net Current Assets is an important figure as it gives an indication of how much cash the business could make available at short notice. Even if a business has a high NAV, if most of its value is tied up in fixed assets it might not be attractive to a potential creditor because it might not have sufficient ready cash to pay bills.

Net Current Assets is now added to Net Book Value of the fixed assets (totalling £54,900 in this example).

The last sub-category of accounts to appear in the top half of the Balance Sheet is long-term liabilities. These are often loans which are not repayable at a time which is more than a year in the future. The total amount of these long-term liabilities (£10,000 in this example) is set out in the right hand column and is used in calculating the NAV.

You can see the final calculation for the top half of the Balance Sheet by reading down the right hand column. The calculation in this example is: FIXED ASSETS (NET BOOK VALUE) 10,600 + NET CURRENT ASSETS 44,300 – LONG TERM LIABILITIES(10,000) = NET ASSETS 44,900

The bottom part of the Balance Sheet shows the funds that have been invested in the business to achieve the total Net Assets. The capital figure represents money contributed by the owners and/or an accumulation of profits from previous accounting periods. The profit figure is the final figure taken from the Profit and Loss Account for the current accounting period. The drawings are withdrawals of capital from the business by the owners and are therefore shown as a deduction.

Having produced the profit and loss account for the period, it is now possible to prepare a Balance Sheet for the period. On its own, the Profit and Loss Account is an incomplete record of a business’s financial position as it only records two income and expenses. The Balance Sheet will record the situation of the business in respect of asset, liability and capital accounts from the trial balance.

The Balance Sheet differs from the Profit and Loss Account as it is a snapshot that is only relevant on a given date. The date at the top of a Balance Sheet is the last day of the accounting period to which it relates. The heading of a balance sheet always contains the words “as at” a specified date. That balance could be different the very next day, if for example, an asset was sold and the proceeds used to pay bills.

The Balance Sheet principally indicates:

the net worth or net asset value (‘NAV’) of the particular business (i.e. the value of the assets it has, less the liabilities it owes). This is recorded in the top half of the Balance Sheet; and

the capital invested in the business to achieve that net worth. This is recorded in the bottom half of the Balance Sheet.

These figures will always be the same, unless something has gone wrong. The two halves of the Balance Sheet must always ‘balance’. This ‘balancing effect’ is because the top half of the Balance Sheet demonstrates how the money invested by the owners of the business has been used.

As a general rule, asset, liability and capital entries from the trial balance are transferred into the Balance Sheet. For example, ‘debtors’ in the trial balance is an asset and this appears in the top half of the Balance Sheet. Compare this to ‘capital at the start of the year’, which is a capital entry and appears in the bottom half of the Balance Sheet.

In my next post, I will present an example of a Balance Sheet, together with notes regarding it.

The trial balance is used by accountants to produce the Profit and Loss Account and the Balance Sheet.

The Profit and Loss Account, which is also known as an Income Statement in international accounting standards, essentially records the income of a business throughout an accounting period minus expenses incurred in that period, to end up with a profit or loss figure for that period. It is therefore a summary of the fortunes of a business over a passage of time. This is why it is vital to note the period to which the Profit and Loss Account relates in order to understand it. The accounting period is recorded in the heading for the account, always with the words “for the period ending on [last day of the period]”.

As a general rule, only the income and expense entries from the trial balance are transferred into the Profit and Loss Account. For example, ‘Commission’ in the trial balance is an income account and this appears at the top of the Profit and Loss Account. In contrast, ‘electricity bill’ is a business expense and appears in the expenses section of the Profit and Loss Account. ‘Cash at bank’, on the other hand, is an asset account and does not appear on the Profit and Loss Account.

There are standard formats for presenting the layout of the Profit and Loss Account and all Profit and Loss Accounts for UK businesses follow a similar structure.

Below is an example Profit and Loss Account for ABC Trading, together with notes to explain its format.

ABC Trading – Profit and Loss Account for the Year Ended [dd/mm/yy]

Notes for the Profit and Loss Account

1. All income entries from the trial balance are put at the top of the Profit and Loss Account (e.g. sales).

2. You will note there is a separate entry labelled ‘Gross profit’ in the top part of the Profit and Loss Account. This figure is not itself taken from the trial balance but is calculated using some entries that are shown on the trial balance.

The ‘Gross profit’ calculation represents all the income of the business less the ‘cost of sales’, that is, costs directly attributable to how the business earns money (e.g. the cost of purchasing stock). The ‘Gross profit’ figure shows the reader how much money the business has made during the accounting period before other expenses are taken into account.

The calculation must be shown in full on the Profit and Loss Account in the format shown in the example.

‘Cost of sales’ includes figures for ‘opening stock’ and ‘closing stock’. These accounts represent the value of unsold stock held by the business at the start and end of the accounting period respectively. (They are asset accounts, so these two accounts are exceptions to the general rule that a Profit and Loss Account shows only income and expense accounts). The figure for closing stock never appears on the trial balance but would be provided separately.

4. All expenses excluding purchases (which have already been deducted in the cost of sales calculation) are deducted from the Gross profit. Such expenses are, broadly speaking, the ‘overheads’ of the business.

5. The resulting figure is the Net Profit and this figure will appear as ‘profit for the year’ in the bottom half of the Balance Sheet

As I wrote in my post on double entry book-keeping, the dual nature of accounting transactions means that for every debit entry there is a matching credit entry and vice versa. It therefore follows that the total of all debit balances in the accounts must always be equal to the total of all credit balances.

To test this out, if we take all the balances on all of a business’s ledgers (i.e. the categories of transaction) as at the end of an accounting period and list them, showing debit balances in one column and credit balances in another column, the total of each of the two columns should be the same. This list is called a trial balance.

Preparation of a trial balance is beyond the scope of the LPC, as a trial balance is usually put together by the business itself or its accountants and forms the basis of information from which the financial statements, principally the Profit and Loss Account and Balance Sheet, are then compiled.

To enable the owners of a business to be able to make sense of its financial performance, it is useful for them to be able helpful to be able to compare the position year-on-year and give them perspective about the profitability of the business on an ongoing basis. This will enable them to make informed decisions about the business.

Therefore, periodically, the ledgers/accounts of a business will be ‘ruled off’ so that the balances on the various accounts can all be looked at together and the finances of the business compared with previous periods. This is done at the end of each accounting period/financial year and many businesses will also prepare ‘interim accounts’ during the course of a financial year.